Global AgriTrends

Back05.22.26

Broken Records (and RAIN in the forecast)

Not only does my beef market commentary sound like a “broken record” suggesting higher prices still ahead, but all classes of cattle continue to also “break records”. If you are not familiar with the term of sounding like a “broken record” ask someone with gray hair to explain…

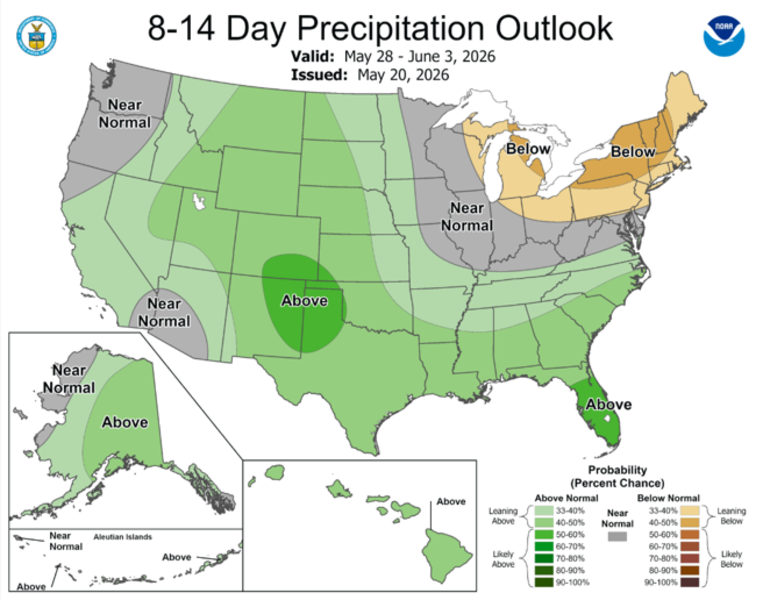

There are lots of moving parts in the beef markets. China reopened to U.S. beef last week, cattle are back at new record highs (still below our forecasted highs), consumers are feeling pinched according to Walmart where lower earnings were blamed on inflation, and Screwworm has kept the Mexican border closed even as cases approach the U.S. The bottom line: tightening supplies are still supportive to higher prices. Tomorrow’s Cattle on Feed report is forecast to show increased total inventories due to slower marketings (and lower placements). Restocking efforts have been halted due to widespread drought but the “Super El Nino” may be beginning with improved rainfall forecast broadly across the key cattle regions over the next 10 days (and next 7 months).

Weekly beef export shipments continue pacing well below year ago levels. Weekly net sales dropped on bookings by Japan, Korea, and Mexico. My Asia travels last week have confirmed how painful these rising beef prices are to the currency-crunched importers in Japan and Korea.

Some thoughts on the current cattle and beef markets:

- Steer and heifer slaughter continues to pace -9% YTD versus a year ago.

- Cargill initiated a worker “lock-out” yesterday at their Fort Morgan plant after the labor union rejected their “last, best, and final” offer (reportedly a $33.4 million increase in wages and benefits). This will not affect cattle flows this week as the plant stopped operations April 23rd. With excess slaughter capacity around the nation, these cattle have easily been absorbed elsewhere.

- Steer carcass weights have held mostly steady YTD averaging 978 pounds, up 28 pounds (+3%) from a year ago.

- Beef imports from Argentina have increased 58% YTD after Trump expanded their quota to 100,000 mt this year. As impressive as that sounds it equates to 11,000 mt in the first five months of the year or 0.1% of U.S. beef consumption this year.

- Cow slaughter continues pacing -5% YTD versus last year.

- Beef production is averaging -5.6% YTD versus a year ago. Even as consumers may be strained by high food and energy inflation, beef supplies are tightening, supportive to prices.

- The comprehensive beef cutout sits at $391/cwt with expected price hikes into seasonal summer demand.

- Fed cattle broke another weekly record averaging $263/cwt thus far this week, up 16% from a year ago. We continue to hold to our forecast from last November with prices peaking in the $270 range mid-year.

- 90% trims are at right even with their record high of $459/cwt this week, up 21% above year ago levels.

- The 8-10 day weather forecast shows improving rainfall across Texas and much of the U.S. The “Super El Nino” is beginning. Rising temps on the equatorial pacific ocean surface are fueling heavy evaporation that fuels the U.S. jet stream. Increased precipitation is likely to accelerate in the 2nd half of 2026. This could lead to very favorable herd-restocking conditions this fall.

- Still no news of a Mexico border opening as New World Screwworm cases are nearing the U.S. border. We expect the border to remain closed.

Bottom line: Cattle and Beef bold

The U.S. beef complex continues to see tightening supplies, supportive to higher prices. Fed cattle and pushing into new record highs, supporting record high feeder and calf prices. Corn remains plentiful and relatively cheap.

Restocking efforts remain muted due to serious drought across the central and southern plains as well as the southeastern U.S. However, these conditions appear to be improving as the “Super” El Nino ramps up (forecast to peak into December).

Americans are likely feeling pinched by higher fuel, food (and everything) costs. Inflation topped 3.8% last month, an uncomfortable rate. Inflation will continue at these higher rates. Walmart released underwhelming earnings yesterday pointing to higher inflation pressure on consumers. Does this matter to beef? Yes, but note that beef production is falling, now down -5.6% YTD. That means the market will allocate these tighter supplies to the highest bidders. And those paying the sustained high beef prices may be most resilient to inflation. The beef and cattle highs are NOT YET IN. History tells us that those highs come the first year that the herd begins growing. That looks like 2027 for now.

My travel and meetings in Japan and Korea last week confirmed how painful high beef prices are to those importers. Japan is particularly pressured. And with our expectation of rising prices out of both Australia and the U.S. into 2027, the winners will likely be pork and chicken. There simply are not any cheap beef options for these currency-stressed importers. And China’s new access to U.S. beef was not good news for Korean and Japanese beef importers. I believe China can outbid Japan for many of those cuts.

The “Super El Nino” impact appears to be beginning with increased precipitation forecast across a broad swath of the U.S. over the next 8-14 days. The Texas drought may be ending. Tough drought conditions have pushed liquidation recently.

Tomorrow’s Cattle on Feed report is expected to show an increase in total cattle on feed as slower placements combine with slower marketings. There’s only one way that is done with a beef cow herd down -12% over the past five years: slow the flow of cattle out of feedyards. That has been manifest by carcass weights up 28 pounds thus far this year. This move creates some short-term supply at the cost of longer-term scarcity.

Brett Stuart